Step 1 – Contact Irish Insolvency Solutions

- If you are finding your debts hard to pay, contact Irish Insolvency Solutions to get professional help from experts in the field.

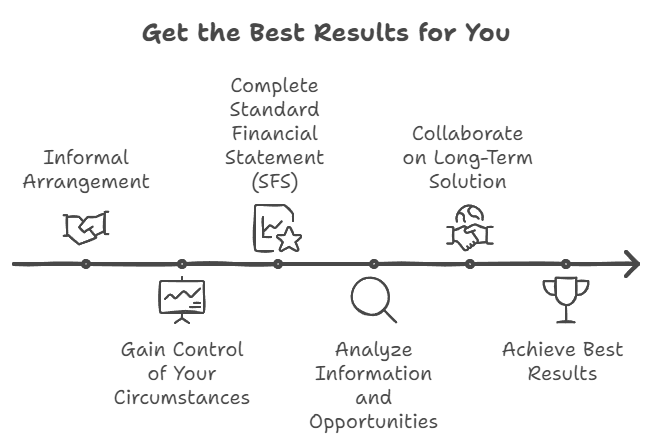

Step 2 – Use this site to inform yourself

- The process are described under ‘Services’ In many cases, an informal arrangement will arrive at the long term solution that will suit your needs

- The ‘Resources’ page gives you some pointers so you can gain control of your circumstances, we believe in working together and assisting you in the process, but encourage you to engage with the facts and details of your circumstances so we can use all the information and opportunities to get the best results for you.

- Banks will require you to complete a Standard Financial Statement (SFS), we have one on this site for each bank and will help you complete the SFS.

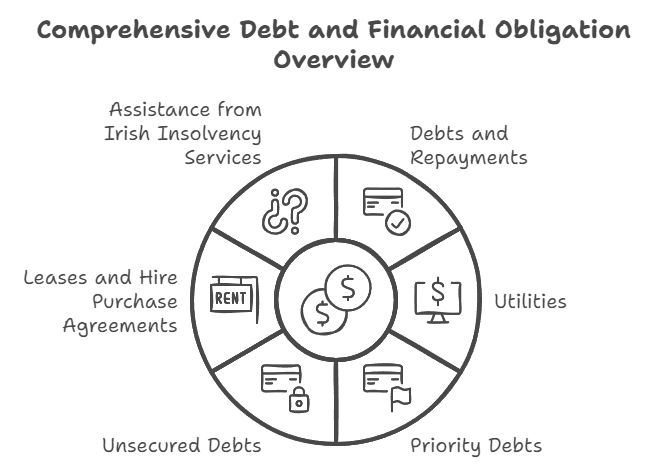

Step 3 – Understand Your Current Position

- Make a list of all your debts and repayments on these debts

- Are any in arrears?

- Do any need immediate attention?

- List your utilities – ESB, Gas, Refuge and Phone

- What is an average monthly bill for each of these

- Are any in arrears – are you at risk of being cut off?

- Identify your Priority Debts – Mortgage & Mortgage Arrears, Rent, Fines, Maintenance – this are very important and have to be seen to get priority attention

- List your Unsecured debts (may also be called Secondary Debts) – typically Overdraft, Credit Cards, Credit Union Loans, Personal Loans, Catalog Accounts etc.

- Did you give the lender/creditor any security against any of these debts?

- Are they all unsecured?

- List any Leases or Hire Purchase Agreements – typically these are for a Car or other costly asset

- The Asset does not become yours until the last repayment is made

- Are any at risk of repossession?

- Irish Insolvency Services will help you understand your current position

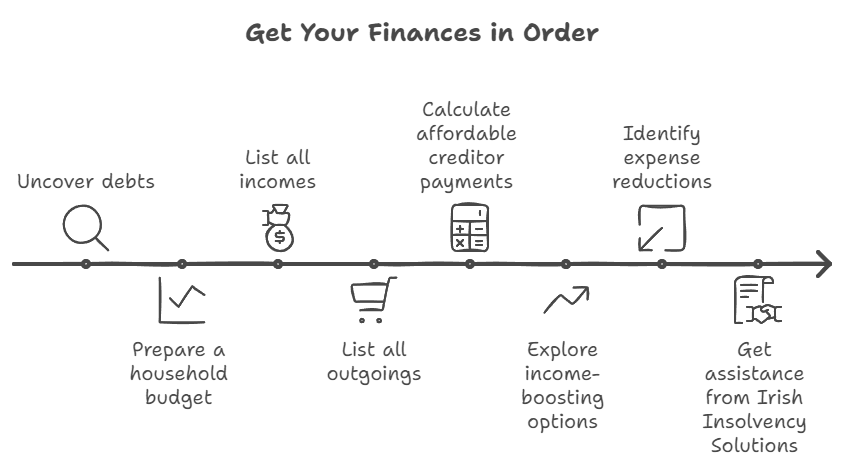

Step 4 – Prepare a Household Budget

- Starting with the debts you uncovered above – prepare a household budget

- List all your incomes from all sources in the house

- List all the current outgoings (try not to leave anything out)

- Within a short space of time you will be able to work out how much you can afford to pay to the creditors listed in Step 1

- To ensure that the Budget Plan is covering your personal circumstances, see if there is anything that may help on the income side:

- Tax Credits – there may be some due to you

- Social Welfare Entitlements – are you claiming all that you can?

- Did you purchase any form of loan protection or insurance that may help?

- Is there a room in the house that could be rented out?

- Your creditors will expect you to make reductions in your expenses – there are areas that could be reduced:

- Phone – ‘bundling’ offers are available that can save you money

- ESB – is there anything that could be saved on the electric bill or from competitors for your electric business? (same for other utilities)

- TV is there a package that will be cheaper for you?

- Have you looked at your life insurance policies, many companies now offer cheaper cover or equal policies for less

- Health Insurance – have you tried to arrange a cheaper offer from a different provider?

- Irish Insolvency Solutions will assist you with your household budget

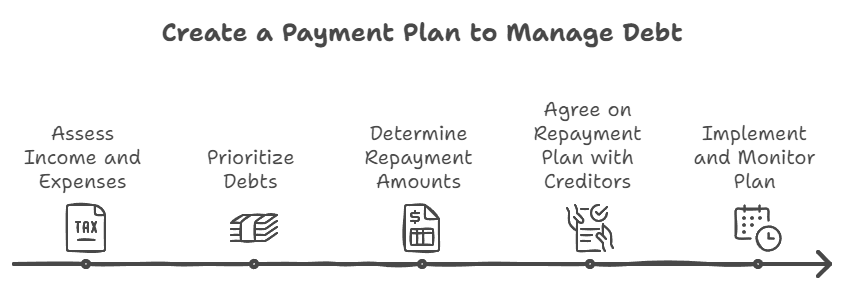

Step 5 – Prepare Your Own Payment Plan

- When all the above steps are completed, you may still find that there is insufficient income to make all the repayments expected of you. You will need to determine a payment plan

- Start with your Priority Debts

- Mortgage, Mortgage Arrears, Rent etc.

- These will receive preferential treatment so that your home isn’t repossessed, you won’t be evicted and the lights can stay on – you can rely on having somewhere to live

- Then add in the secondary debts

- Based on what is left from the income and expenditure budget work out what can be paid to each loan/creditor.

- A monthly repayment plan will need to be agreed with all of your creditors.

- It is important to keep something for all creditors each month so that legal action is not precipitated by any disgruntled creditor.

- Irish Insolvency Solutions will assist you in preparing your payment plan

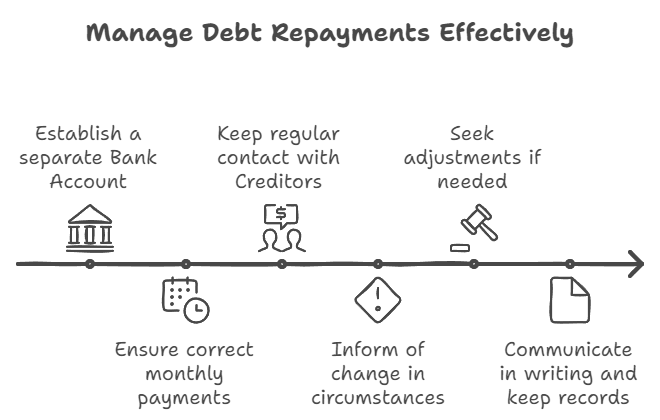

Step 6 – Show Financial Management and Control of Your Circumstances

- Establish a distinct separate Bank Account to make what you budgeted under repayments

- Ensure that the correct amount goes into this account each month

- Stick to the Plan

- Know how to, and then keep regular contact with your Creditors

- Inform them of a change in circumstances immediately

- Adjustments are possible if everyone knows what is going on and feels they are being treated fairly (in advance if possible)

- All communication with your creditors should be in writing and a copy of all correspondence should be kept in a safe place

Other Resources

Where necessary, at a clients instruction or to cater to a clients wishes we have a number of professional resources that can be introduced to our processes. Irish Insolvency Solutions has access to Legal, Financial and Strategic Planning experts across the country. These professionals, where required, provide an excellent resource and support to our clients in matters concerning

- Legal Advice

- Tax Advice

- Financial Planning

- Business Planning

- Strategic Communications

In whatever circumstance our clients find themselves, we can offer the correct professional advice to manage the situation and to find the best results.

Standard Financial Statements (SFS)

AIB SFS – Read

AIB MARP – Read

BOI SFS – Read

BOI MARP – Read

BCM Global SFS – Read

BCM Global MARP – Read

Cabot Ireland Financial SFS – Read

Cabot Ireland Financial MARP – Read

Link Financial SFS – Read

Link Financial MARP – Read

MARS Capital SFS – Read

MARS Capital MARP – Read

Pepper SFS – Read

Pepper MARP – Read

PTSB SFS – Read

PTSB MARP – Read